Why Buffett’s Index Fund Bet Still Beats Wall Street: The Hidden Geometry of Modern Markets and the Rise of Algorithmic Trading

Warren Buffett’s famous index fund bet revealed a deeper truth about modern markets: despite high-frequency trading, hedge funds, and AI-driven strategies, passive investing continues to outperform most active managers. This analysis explores market microstructure, arbitrage, Jim Simons’ quant revolution, and why efficiency—not inefficiency—explains why “doing nothing” still wins in global finance.

5/17/20264 min read

The Hidden Geometry of Markets: Why Buffett’s “Do Nothing” Bet Keeps Winning in a Hyperactive Trading World

Introduction: A Million-Dollar Bet That Exposed Wall Street’s Core Paradox

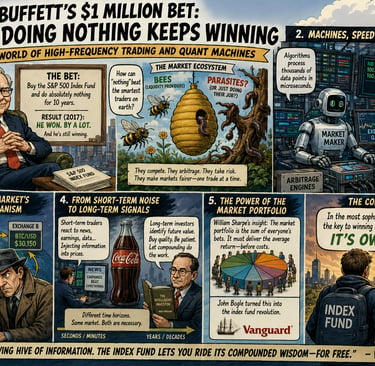

In 2007, Warren Buffett placed a $1 million wager on what looked like the most naïve strategy in modern finance: buy a broad basket of equities and do absolutely nothing for a decade.

No alpha generation. No timing the Fed. No hedge fund wizardry. No leverage. Just passive exposure to the U.S. equity market.

A decade later, the result wasn’t close.

The evidence suggests something uncomfortable for active managers: the average investor, stripped of fees, friction, and emotional overtrading, tends to outperform even the most sophisticated Wall Street professionals over long horizons.

From a boots-on-the-ground perspective in today’s markets—where algorithms execute trades in microseconds and liquidity is manufactured by machines—the paradox deepens:

How can “doing nothing” consistently beat an industry built on doing everything?

The Trading Ecosystem: Parasites, Bees, or Market Infrastructure?

There is a long-standing moral narrative in finance:

Active traders are either parasites extracting value

Or “bees” improving price discovery

The reality is more mechanical—and more brutal.

Modern markets, especially in the U.S. equity ecosystem centered around Wall Street and the Federal Reserve-driven macro regime, function as an information-processing system. Every participant—retail, hedge funds, quant firms, market makers—feeds signals into prices.

The key shift over the last two decades is that most of this processing is no longer human.

It is algorithmic.

And that changes everything.

Liquidity Is Not a Given—It Is Manufactured

A core misunderstanding among non-professionals is that markets are naturally liquid.

They are not.

Liquidity is created by competing incentives:

Market makers quoting bid/ask spreads

High-frequency traders arbitraging price differences

Statistical arbitrage funds balancing relative mispricings

Without these actors, even modest orders would cause extreme price dislocations.

A historical analogy helps clarify this:

In the 1980s, large institutional orders in stocks like IBM could move prices by 5–8% in a single print due to shallow order books.

Today, that same order is absorbed almost invisibly due to algorithmic liquidity provision.

The evidence suggests something counterintuitive:

The “parasites” are actually stabilizers.

But they are not doing it out of altruism—they are extracting micro-profits from speed and information asymmetry.

The Order Book Reality: Where Microstructure Creates Opportunity

Modern exchanges like those in the Nasdaq ecosystem operate through order books:

Buy orders (bids)

Sell orders (asks)

Limit orders sitting at various price levels

A market order doesn’t “find a fair price.” It consumes liquidity.

This is where slippage emerges—the hidden tax on urgency.

In thin markets (crypto in its early cycles is a perfect example), this structure breaks down:

Liquidity gaps appear

Prices diverge across venues

Arbitrage opportunities emerge temporarily

But these inefficiencies are self-correcting.

Because once identified, they attract capital instantly.

Crypto’s Early Chaos: A Live Experiment in Inefficient Markets

During the 2017 crypto cycle, exchanges were fragmented and uneven:

Same asset, different prices across venues

Thin order books with unpredictable depth

Latency-driven arbitrage opportunities

The evidence suggests this phase wasn’t unique to crypto—it was simply a compressed version of what all markets look like before institutional capital arrives.

A boots-on-the-ground perspective from that environment reveals a simple truth:

If you could see the mispricing, so could someone faster, better capitalized, or closer to infrastructure.

That’s the real edge: not discovery, but speed of execution.

Arbitrage: The Market’s Self-Healing Mechanism

At its core, arbitrage is not “free money.”

It is the mechanism by which markets enforce consistency.

Across:

Exchanges

Asset pairs (e.g., Coca-Cola vs PepsiCo)

Derivatives vs spot markets

Mispricings act like geometric distortions in a system that constantly seeks equilibrium.

Think of it this way:

If two identical assets diverge in price, capital flows in to exploit the gap

That flow eliminates the gap

Profit exists only until it is discovered

This is why firms like D. E. Shaw and Renaissance Technologies scaled statistical arbitrage into multi-billion-dollar strategies.

They weren’t predicting markets.

They were correcting them.

The Buffett Insight: You Don’t Need to Win the Game to Win the Outcome

The intellectual pivot comes from reframing markets not as a battlefield, but as a weighted average of all participants.

This is where portfolio theory enters. The market portfolio—the aggregate of all holdings—naturally reflects collective capital allocation decisions.

This idea was formalized in modern finance theory and later popularized through passive investing vehicles like index funds created by Vanguard under the philosophy of John C. Bogle.

The implication is brutal:

Active traders compete against each other

The average result is the market return

Fees, friction, and errors push most active strategies below that average

So the index wins not because it is smarter—but because it refuses to lose to itself.

Jim Simons and the Final Stage: Markets as Geometry

At the highest level of sophistication, markets stop looking like narratives.

They become geometry. Jim Simons built an entire investment empire on this idea:

Prices are points in high-dimensional space

Relationships form curved surfaces

Profit exists where prices deviate from equilibrium geometry

When those surfaces shift—due to macro data, flows, or sentiment—algorithms exploit the drift back to statistical norm.

Importantly:

No story is required

No macro thesis is necessary

Only pattern stability matters

But the edge decays fast. Once discovered, it is competed away.

The Real Paradox: The More Efficient Markets Become, the Less You Should Trade

Here is the uncomfortable conclusion:

More participants improve price accuracy

More algorithms reduce mispricing duration

More capital compresses alpha

So paradoxically: The better markets become at pricing information, the harder it becomes for any individual to outperform them. That is why Buffett’s original bet still works. Not because markets are inefficient. But because they are too efficient for most participants to beat after costs.

Skin in the Game Reality Check

From an investor’s standpoint, this creates a psychological trap:

Activity feels like control

Trading feels like intelligence

Inaction feels like ignorance

But the data structure of markets punishes that instinct. Most losses in active trading don’t come from bad ideas—they come from:

Overconfidence in timing

Fee drag

Execution errors

Behavioral reaction to volatility

Meanwhile, passive exposure compounds quietly in the background.

No drama. Just drift.

Conclusion: The Market Is Not Beaten—It Is Joined

The deepest insight from modern financial structure is not that traders are wrong.

It’s that they are collectively right in aggregate—and individually expensive to be.

Markets today are not a casino, nor a machine, nor a conspiracy. They are a continuously self-correcting information network where every inefficiency is temporary and every edge is contested.

In that world, Buffett’s logic becomes almost uncomfortable in its simplicity: The optimal strategy is not to outthink the system—but to own it.

Book Recommendation

If you want to go deeper into the structure behind all of this, read “The Man Who Solved the Market” by Gregory Zuckerman. It provides one of the clearest accounts of how quantitative finance evolved from intuition-driven trading into a machine that interprets markets as mathematical structure rather than narrative.

Link: https://amzn.to/4fra1nd