The Petrodollar System Explained: How U.S. Dollar Dominance Is Being Challenged by De-Dollarization and Global Financial Fragmentation

A deep macroeconomic analysis of the petrodollar system, SWIFT sanctions, dollar dominance, and the growing global shift toward de-dollarization, gold accumulation, and alternative trade currencies.

5/15/20264 min read

The Petrodollar System: How a 50-Year Financial Architecture Is Being Stress-Tested

Introduction: The Invisible Infrastructure Behind Global Power

The global financial system doesn’t run on trust alone—it runs on design. And few designs have been as consequential as the petrodollar system.

What began as a geopolitical workaround in the 1970s has evolved into a structural pillar of U.S. economic power, shaping everything from Treasury demand to military projection and global liquidity. But today, that architecture is being questioned in ways that feel less theoretical and more operational.

A boots-on-the-ground perspective reveals a system that still dominates—but is no longer uncontested.

The Collapse of Bretton Woods and the Birth of “Trust-Based Money”

The modern dollar system begins with a rupture.

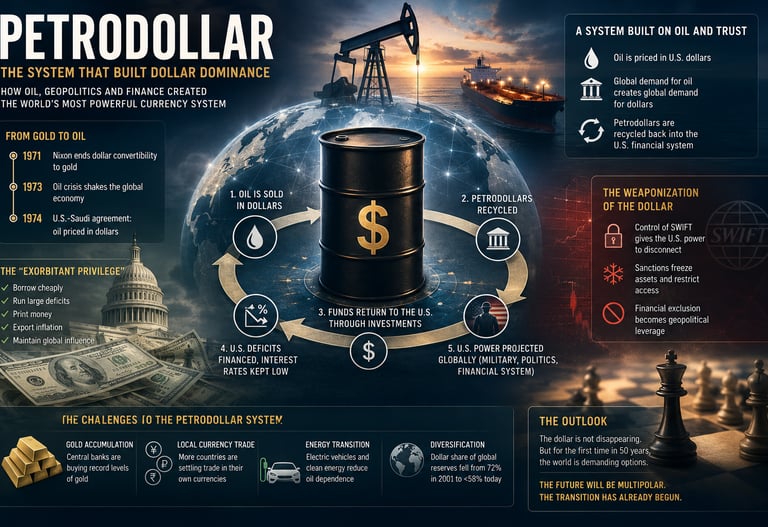

In 1971, the U.S. ended the dollar’s convertibility into gold under President Nixon. The system built at Bretton Woods had become unsustainable: America had issued more dollars than it could realistically back with gold reserves, largely due to war spending, domestic programs, and Cold War commitments.

The result was a currency no longer anchored to a physical commodity, but to something far more abstract: confidence.

The evidence suggests that this moment was not just monetary—it was existential for the dollar. Without gold backing, the U.S. needed a new form of structural demand. That demand arrived through oil.

The Petrodollar Deal: Oil as Monetary Anchor

In the mid-1970s, a strategic agreement with Saudi Arabia reshaped global finance. Under this framework, oil would be priced and traded primarily in U.S. dollars. In return, oil-exporting nations gained security guarantees and access to U.S. financial markets.

This created a powerful loop:

Global oil demand → global dollar demand

Oil revenues → recycled into U.S. financial assets

Capital inflows → funding for U.S. deficits and liquidity expansion

This is the essence of the “petrodollar recycling” mechanism. A boots-on-the-ground perspective reveals the simplicity behind the complexity: if every industrial economy needs oil, and oil is priced in dollars, then everyone needs dollars—regardless of trade balance.

The Recycling Engine: Why Global Surpluses Flow Back to Wall Street

Oil exporters often accumulate more dollars than they can reinvest domestically. That surplus does not sit idle.

Instead, it is typically recycled into:

U.S. Treasury securities

American banking institutions

Equity and credit markets in the United States

This creates structural demand for U.S. debt instruments, helping:

Finance federal deficits at lower borrowing costs

Stabilize Treasury auctions

Anchor global liquidity inside U.S. financial markets

The system is self-reinforcing. Oil generates dollars; dollars return to fund U.S. fiscal capacity. The implication is clear: U.S. debt markets are not just domestic—they are global infrastructure.

The “Exorbitant Privilege”: When Currency Becomes Power

Economists have long referred to the dollar’s role as an “exorbitant privilege.”

In practical terms, this includes:

Lower borrowing costs for U.S. government debt

Persistent global demand for dollar reserves

Ability to run structural deficits without immediate currency collapse

Exporting part of inflation pressure abroad

The evidence suggests this is not merely financial convenience—it is geopolitical leverage embedded in monetary structure.

When capital markets, commodities, and reserves all converge on a single currency, monetary policy becomes global policy.

SWIFT and Sanctions: The Financial “Switch” of the Modern Era

If the petrodollar is the system’s foundation, SWIFT is its operating layer. SWIFT is not a bank or payment processor—it is messaging infrastructure that allows global banks to coordinate transactions. Being excluded from it is not symbolic. It is functional isolation.

Sanctions tied to this infrastructure allow the U.S. and allies to:

Freeze foreign reserves held abroad

Restrict international trade settlement

Disrupt banking connectivity

Force compliance through financial isolation

The most cited modern example is Russia in 2022, when major financial institutions were cut off and large portions of foreign-held reserves were immobilized.

From a systems perspective, this is equivalent to being disconnected from global financial plumbing.

The Strategic Shock of 2022: When “Safe Assets” Became Conditional

The freezing of sovereign reserves introduced a psychological shift in global central banking. A key assumption was broken: that dollar reserves were neutral, apolitical, and fully accessible. After 2022, that assumption no longer held.

The evidence suggests a structural response followed:

Increased central bank gold purchases

Reduced exposure to U.S. Treasuries in some portfolios

Expansion of bilateral trade settlement in local currencies

Exploration of alternative payment rails outside SWIFT

This is not a coordinated rebellion. It is risk management.

De-Dollarization: Fragmentation, Not Replacement

Despite headlines, the dollar has not been replaced. It has been challenged at the margins.

Key trends include:

China reducing Treasury exposure while increasing gold reserves

Russia accelerating non-dollar settlement mechanisms

India and Brazil expanding local-currency trade frameworks

Saudi Arabia signaling flexibility in oil pricing currencies

But the system remains structurally dominant:

The dollar still accounts for the majority of FX transactions

Global debt markets remain heavily dollar-denominated

U.S. Treasury securities are still the primary reserve asset class

A boots-on-the-ground perspective reveals the real story: not collapse, but gradual fragmentation at the edges of a still-central system.

Energy Transition: The Slow Structural Pressure Point

One of the more underappreciated dynamics is energy transition. As electric vehicles and alternative energy sources expand, oil demand growth slows relative to historical trends.

If oil is the anchor commodity of the petrodollar system, then reduced oil centrality implies reduced structural dollar demand.

The evidence suggests this is a long-cycle risk, not a near-term shock—but it matters at the system level.

The Core Contradiction: Stability Built on Strategic Force

The petrodollar system contains an internal tension.

On one hand, it provides:

Deep liquidity

Global trade efficiency

Stable reserve assets

Predictable capital recycling

On the other hand, it relies on:

Geopolitical enforcement

Financial exclusion mechanisms

Selective access to infrastructure

The more the system is used as a tool of coercion, the more incentives other actors have to reduce dependency on it. This is the paradox at the heart of modern dollar power.

Conclusion: A System Under Gradual Repricing

The dollar is not losing dominance in a linear way. It is being repriced. What we are observing is not a replacement of the system, but a diversification away from single-point dependency—across reserves, trade settlement, and financial infrastructure.

From a macro investor’s perspective, the key question is not whether the dollar survives. It clearly does.

The real question is what premium global markets are willing to assign to U.S. monetary centrality in a world where alternatives, while imperfect, are no longer theoretical.

A boots-on-the-ground perspective suggests the answer is evolving in real time.

Recommended Book

For a deeper understanding of how currency systems evolve into geopolitical power structures, a strong reference is “Exorbitant Privilege” by Barry Eichengreen. It explains how the dollar achieved dominance and why structural inertia—not just economic strength—keeps reserve systems in place long after their original con;ditions change.

Link: https://amzn.to/4uk6sEc