The Crash of 1929 Explained: How Easy Money, Leverage, and Wall Street Greed Triggered the Great Depression

Discover how the 1929 stock market crash was built on cheap credit, leverage, speculative excess, and Federal Reserve policy. A deep macroeconomic analysis connecting the lessons of Wall Street's greatest collapse to today's markets.

6/19/20265 min read

The Crash of 1929: When America Mistook a Bubble for a New Economic Era

Every Generation Believes the Rules Have Changed

The trading floor was deafening.

Telephones rang endlessly. Brokers shouted over one another. Price tickers printed numbers that, by that point, barely reflected reality. Inside Wall Street, investors dumped assets at any available price. Outside, crowds gathered in disbelief, trying to understand where a lifetime of savings had disappeared.

October 1929 was not simply a stock market crash. It was the violent end of a decade-long experiment built on leverage, easy credit, financial engineering, and a dangerous conviction that prosperity had become permanent.

Nearly a century later, the lesson remains uncomfortable: bubbles rarely emerge from ignorance. They emerge from collective confidence.

And confidence, when amplified by cheap money, can become one of the most destructive forces in financial history.

The Birth of America's Prosperity Machine

The Roaring Twenties did not begin with speculation.

They began with genuine innovation.

Following World War I, the United States emerged as the world's dominant industrial power while Europe struggled to rebuild shattered economies. American factories became more productive, corporate profits surged, and transformative technologies entered everyday life.

The economy was being reshaped by:

Electrification

Mass automobile production

Radio adoption

Telephone networks

Consumer appliances

Industrial automation

From an investor's perspective, the optimism was understandable. Economic growth was real. Corporate earnings were rising. Productivity was accelerating.

The evidence suggested that America had discovered a new engine of wealth creation.

The problem was that investors began confusing economic progress with unlimited asset appreciation.

Those are not the same thing.

Credit Became the Most Important Product in America

The defining innovation of the 1920s was not the automobile. It was debt.

For the first time, millions of Americans could purchase products they could not immediately afford. Cars, refrigerators, household appliances, and eventually stocks became accessible through financing.

A boots-on-the-ground perspective reveals something important about every financial bubble: people rarely become reckless overnight.

Instead, debt gradually becomes normalized. Then celebrated. Then expected. Eventually, borrowing becomes the default mechanism for wealth creation.

That is exactly what happened in the United States. Margin investing exploded.

Investors frequently purchased stocks by contributing only 10% to 20% of the capital themselves while borrowing the remainder from brokers.

Broker loans expanded dramatically throughout the decade, creating an enormous layer of hidden fragility beneath the market's spectacular gains. As long as prices rose, the system appeared brilliant. Once prices stopped rising, the structure became lethal.

The Federal Reserve's Small Decision With Massive Consequences

History often turns on decisions that appear insignificant at the time. One of those moments occurred in 1927. Federal Reserve officials lowered interest rates and expanded liquidity at a moment when speculation was already accelerating.

The move was intended to support economic stability. Instead, it poured fuel onto an already growing fire. Cheap money changed investor behavior.

Why lend capital conservatively when stock prices appeared to rise every month?

Why invest in productive capacity when financial speculation generated faster returns?

Sound familiar?

Investors who lived through the dot-com bubble, the housing bubble, or the era of near-zero interest rates after 2008 have seen this movie before. Different assets. Different technologies. The same psychology.

Wall Street's Original Financial Engineering Boom

Many people assume modern financial engineering began with derivatives or mortgage-backed securities.

It didn't.

The 1920s had their own versions. Investment trusts, holding companies, and highly leveraged corporate structures proliferated throughout the decade.

These entities often owned other entities, which owned additional entities, creating layers of leverage that amplified gains during good times.

The result was a financial system increasingly disconnected from productive economic activity. Money was generating money.

At least on paper. The danger was that much of the apparent wealth depended entirely on rising asset prices.

Once that assumption failed, the entire structure became unstable.

The Cult of Optimism

One of the most overlooked drivers of financial crises is social pressure. By 1929, optimism had become America's dominant ideology. Questioning the market was viewed as backward. Warning about risk was considered foolish.

Skeptics were ridiculed. Believers were rewarded. Economists, bankers, journalists, politicians, and investors increasingly shared the same assumption:

This time was different. The most dangerous phrase in investing is not "buy the dip." It is "the old rules no longer apply."

Every bubble eventually adopts some version of that belief. The dot-com era had the internet. The housing bubble had real estate.

Today, many investors argue that artificial intelligence, passive investing, or mega-cap technology dominance have permanently changed valuation frameworks. Perhaps some aspects have changed. Human nature has not.

When the Smart Money Starts Leaving

One of the most revealing features of major market tops is that public enthusiasm often peaks after sophisticated investors have already begun reducing risk.

By late 1929, warning signs were becoming increasingly visible. Industrial production weakened. Freight volumes declined.

Credit conditions tightened. International financial stresses intensified. Yet public participation remained strong.

Why?

Because investors rarely evaluate markets based on fundamentals during bubbles. They evaluate them based on recent price action. If prices continue rising, concerns appear irrelevant.

The evidence suggests that markets become most vulnerable precisely when confidence becomes universal. At that point, there are very few buyers left.

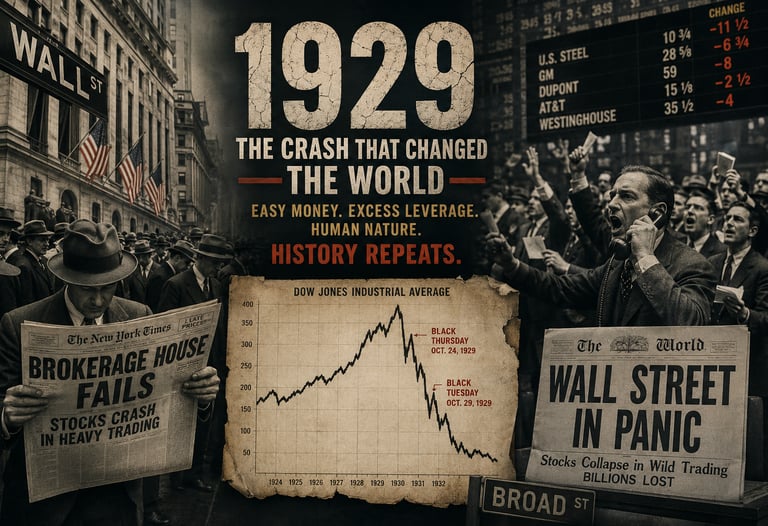

Black Thursday and Black Tuesday

The collapse did not happen because investors suddenly discovered bad news. The bad news had existed for months. The crash happened because confidence disappeared.

Once margin calls accelerated, investors were forced to liquidate positions regardless of price.

That distinction matters. Financial crises often become self-reinforcing. Falling prices trigger forced sales. Forced sales create lower prices.

Lower prices generate additional margin calls. The cycle feeds itself. During Black Thursday and Black Tuesday, the market entered exactly this type of downward spiral.

Liquidity vanished. Price discovery failed. Panic replaced analysis. The market was no longer operating according to valuation models.

It was operating according to fear.

The Real Disaster Came After the Crash

Many investors focus exclusively on October 1929. That misses the larger story. The stock market crash was not the catastrophe. The economic collapse that followed was.

The destruction of financial wealth triggered a chain reaction throughout the economy:

Bank failures surged

Credit availability collapsed

Consumer spending contracted

Corporate bankruptcies increased

Unemployment exploded

International trade deteriorated

By 1933, roughly one-quarter of the American workforce was unemployed. What began as a financial crisis evolved into a social and political crisis and eventually, a geopolitical one.

Why 1929 Still Matters in 2026

The temptation is to view 1929 as an ancient event with little relevance today. That would be a mistake. The specific instruments have changed. The underlying dynamics have not.

Today's markets feature:

Record concentrations in mega-cap technology companies

Extraordinary faith in artificial intelligence

High public market participation

Heavy dependence on central bank policy

Significant asset-price sensitivity to liquidity conditions

None of these factors guarantee a crash.

But they should remind investors that financial history is cyclical. The lesson of 1929 is not that capitalism fails. The lesson is that investors repeatedly underestimate risk during periods of prosperity.

Human beings are wired to extrapolate recent success indefinitely into the future.

Markets punish that behavior eventually. Every generation creates its own version of the "new era." Every generation eventually discovers that economic gravity still exists.

Final Thoughts: The Bubble Never Changes, Only the Story Does

The ultimate lesson of 1929 has little to do with stocks. It has everything to do with human nature. Regulators can reform markets. Central banks can stabilize liquidity. Governments can redesign institutions.

What nobody has ever successfully regulated is greed, optimism, and the belief that easy money can create permanent prosperity.

A boots-on-the-ground investor understands that markets are driven by narratives as much as fundamentals.

The narrative of 1929 was that America had entered a permanent age of wealth. The narrative of 2008 was that housing prices could not decline nationally. The narrative of every future bubble will sound different.

But underneath, the mechanics will be familiar. Credit expands. Leverage increases. Risk becomes invisible and someone, somewhere, becomes convinced that this time is different. It never is.

Recommended Reading

For readers seeking the most comprehensive account of the 1929 crash and the personalities who shaped it, Andrew Ross Sorkin's 1929 is an essential read. Beyond the financial data, the book explores the psychology, political influence, and institutional failures that transformed a market correction into the defining economic disaster of the twentieth century.