The AI Trap: Are You Buying Innovation or Just Overpriced Chips?

4/17/20263 min read

The Tech Dichotomy of 2026: Between Semiconductor Euphoria and Software Discounts

The technology sector in the U.S. markets began 2026 under heavy volatility. After a period of sharp declines, we have seen a recent recovery that raises a fundamental question for any asset allocator: is there still room to buy, or have we reached the top?

A recent report from Goldman Sachs, released on April 10, shed light on this scenario. As an analyst, I see a landscape rarely witnessed in the market: the valuation premium of the "Big Five" tech giants has retreated to levels nearly identical to the rest of the market. Globally, the P/E (Price-to-Earnings) ratio for certain tech segments is currently below that of the consumer and industrial sectors—sectors that historically deliver much lower growth.

The Earnings Engine: AI as an Accounting Reality

We aren't just talking about promises anymore. Goldman estimates that AI investment will account for approximately 40% of the S&P 500's EPS (Earnings Per Share) growth in 2026. Profits remain strong and rising, yet prices haven't always kept pace. However, to invest wisely, one must separate the wheat from the chaff within the sector.

Electronics vs. Services: Where is the Asymmetry?

To understand current opportunities, we must divide technology into two distinct blocks: Infrastructure (Electronics/Semiconductors) and Services (Software).

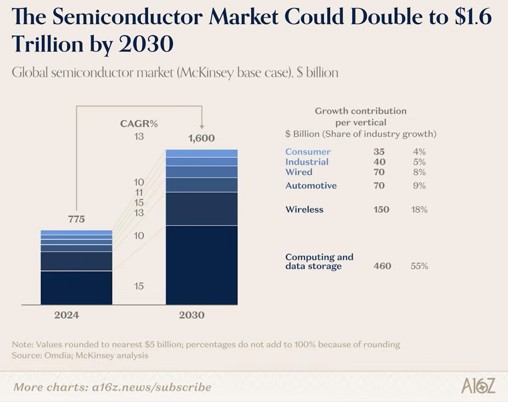

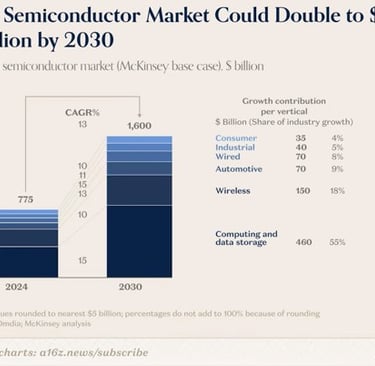

1. Semiconductors (The SOXX ETF Case)

Chip manufacturers are the physical foundation of the AI revolution. Assets like Nvidia, Broadcom, and Micron have seen vertiginous valuations. The SOXX ETF, for instance, surged nearly 35% in the first four months of 2026 alone.

The Analyst’s View: Here, the market is paying a premium. With Micron up 60% and AMD up 30% YTD, the sector is trading near historical highs. Investors here must firmly believe in the continuation of the aggressive Capex cycle in infrastructure through 2030. Currently, semiconductors trade at a multiple 3.5 times higher than the software sector.

2. Software as a Service (The IGV ETF Case)

While chipmakers are soaring, the Software (SaaS) sector has struggled. The IGV ETF fell by roughly 20% in 2026. Why the disparity? The market fears that AI agents (such as Claude and other autonomous models) will replace expensive traditional software licenses, such as those from Salesforce.

The Disruption Risk: In the first quarter of 2026, 27 public companies listed "AI agents" as a competitive risk in their reports—up from just one in early 2024. Are we facing a "Kodak moment" or a generational buying opportunity?

Case Studies: Microsoft and Adobe

Microsoft (MSFT): The Reinventing Giant

Microsoft saw its shares pull back about 13% in 2026, moving away from its highs. However, the accounting fundamentals remain rock-solid: growing revenue, rising profits, and enviable cash flow. The point of concern is Capex, which has tripled since 2022.

Insight: In 2014, the market punished Microsoft for its high investment in the Cloud (Azure). Ten years later, the stock had risen over 700%. Current AI spending seems to follow the same rationale: sacrificing short-term margins for generational dominance.

Adobe (ADBE): Resilience or Obsolescence?

With a 30% drop YTD, Adobe reflects market anxiety. Tools like MidJourney and Sora threaten the reign of Photoshop and Premiere. However, Adobe possesses an ecosystem and customer loyalty comparable to Apple’s. The company is integrating AI as a native feature rather than a separate product. It is a bet on rebranding and technological adaptation.

Conclusion: The "Secret Sauce" for Investors

The tech sector, as a single block, is not necessarily cheap. SOXX is stretched, while IGV is discounted but carries disruption risks.

The true opportunity for 2026 may not lie solely with the companies creating the technology, but with those outside the tech sector that are implementing AI to slash costs and boost margins. There are hundreds of companies in the S&P 500 delivering consistent results, benefiting from technological efficiency, which the market has yet to price as "AI winners."

The Verdict: The dollar is currently at attractive levels for international allocations. The key is not to flee the market because it recovered, but to know how to rotate capital to where value hasn't been fully realized—whether in resilient software players or highly efficient traditional companies.

Did you find this analysis helpful? Leave a comment below: which subsector do you believe will outperform in the second half of 2026—Semiconductors or Software?