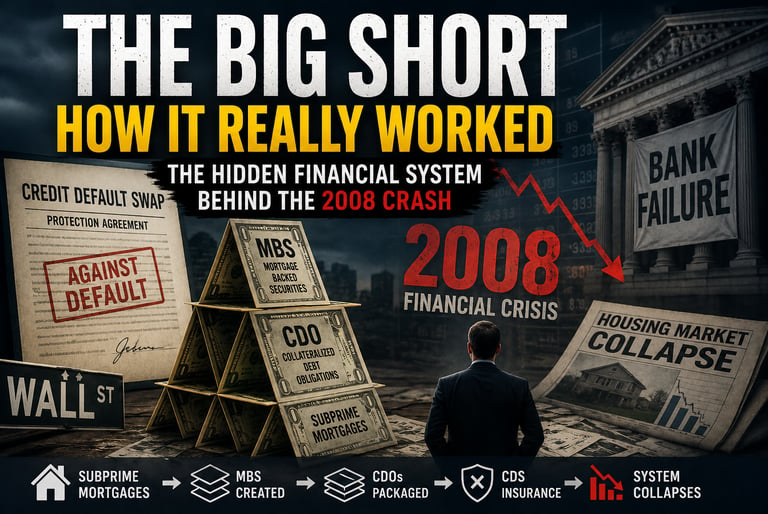

How The Big Short Really Worked — The Hidden Financial System Behind the 2008 Crash

Behind The Big Short was a complex financial system built on leverage, mortgage-backed securities, and hidden risk. This article explains how investors like Michael Burry used Credit Default Swaps to bet against the housing market before the 2008 financial crisis — and why the collapse of Wall Street changed global finance forever.

5/9/20265 min read

How “The Big Short” Really Worked — The Financial Mechanics Behind the 2008 Collapse

Few Hollywood movies have ever explained Wall Street as effectively as The Big Short. While most finance films focus on excess, luxury, and scandals, The Big Short stood out for showing how the global financial system actually operated before the 2008 collapse.

But the real story behind the movie is even more complex — and arguably far more terrifying.

Behind the scenes were exotic financial instruments, hidden leverage, insurance-like derivatives, and a housing bubble so fragile that a small group of investors realized the entire system could eventually implode.

This is how The Big Short really worked.

The Real Investors Behind The Big Short

The film followed three major groups of investors who identified the weaknesses inside the U.S. housing market years before the crash became obvious.

Michael Burry — The First Investor to See the Collapse

Michael Burry

Michael Burry, founder of Scion Capital, was among the first investors to realize that the American housing market was built on increasingly dangerous subprime mortgages.

Contrary to the movie’s simplified narrative, Burry was not an unknown outsider suddenly making a lucky prediction.

Before betting against the housing market, he had already built an impressive investment track record, generating average annual returns of roughly 25% through his hedge fund.

What made Burry different was his willingness to deeply analyze mortgage data that most institutions ignored.

Eventually, he concluded that the entire mortgage-backed system was far riskier than Wall Street believed.

What Were Credit Default Swaps (CDS)?

One of the most important concepts in the movie is the Credit Default Swap, or CDS.

In simple terms, a CDS functioned like financial insurance. Investors paid recurring premiums to banks or insurers in exchange for protection if certain financial assets collapsed.

The genius of Burry’s strategy was realizing he could buy insurance on assets he did not actually own.

It was similar to purchasing fire insurance on someone else’s house — betting that the property would eventually burn down.

When mortgage securities began failing, those CDS contracts exploded in value.

Why Traditional “Short Selling” Wouldn’t Work

Unlike stocks, investors could not simply borrow and short-sell the housing market directly.

Nobody could realistically “borrow a house” and sell it into the market.

That logistical limitation forced investors like Burry to use derivatives instead of traditional short positions.

Credit Default Swaps became the perfect instrument for betting against mortgage-backed securities without needing to physically own the underlying assets.

Mortgage-Backed Securities (MBS): The Foundation of the Crisis

At the center of the crisis were Mortgage-Backed Securities, commonly known as MBS.

Banks pooled thousands of mortgages together into large financial products that investors could buy.

The idea seemed simple:

homeowners made mortgage payments

investors received income from those payments

banks created more liquidity to issue new loans

For years, the system appeared stable.

But underneath the surface, lending standards were collapsing.

Subprime borrowers with weak financial profiles were receiving mortgages they could not realistically afford long term.

The Dangerous Illusion of “Safe” Tranches

To make these securities more attractive, Wall Street divided them into layers called tranches.

Think of it like buckets in a waterfall.

The first bucket received payments first and was considered safer.

The final bucket received whatever remained, offering higher returns but carrying far more risk.

This structure created the illusion that certain mortgage investments were extremely secure — even when the underlying loans were weak.

Rating agencies often assigned high credit ratings to these upper tranches, convincing pension funds and institutions to buy them aggressively.

CDOs: The Financial System Became a Machine Built on Debt

Wall Street eventually pushed the system even further through products called Collateralized Debt Obligations (CDOs).

Collateralized Debt Obligation Instead of containing simple mortgages, CDOs bundled together multiple Mortgage-Backed Securities into even larger products.

The theory was that diversification would reduce risk.

In reality, it created massive interconnected fragility.

Eventually, firms even created “CDO squared” structures — products built from the riskiest parts of other CDOs.

At that point, the financial system became so interconnected that a nationwide decline in housing prices threatened the entire global banking system.

Why Diversification Failed in 2008

One of the biggest lessons from the financial crisis is that diversification alone cannot protect against systemic collapse.

The system assumed that housing markets across America would never fail simultaneously.

That assumption proved catastrophically wrong.

When mortgage defaults began rising nationally, the entire cash flow structure supporting MBS and CDOs started collapsing at once.

The diversification that supposedly made the system safe became meaningless.

The Risk Nobody Talks About: Counterparty Collapse

Even after investors like Michael Burry were proven correct, another major danger emerged.

What if the institutions selling the insurance could not actually pay?

Companies like AIG had issued enormous amounts of Credit Default Swaps without fully understanding the scale of potential losses.

As the housing market collapsed, investors feared that the counterparties behind the CDS contracts might themselves become insolvent.

That is why many of the investors portrayed in The Big Short sold their contracts back to banks before the entire financial system completely froze.

They locked in profits before the insurers themselves potentially failed.

What The Movie Changed About Michael Burry

Although The Big Short is praised for technical accuracy, several details were simplified for storytelling purposes.

1. Burry Didn’t Invent CDS

The movie gives the impression that Burry pioneered Credit Default Swaps.

In reality, CDS contracts had already existed since the 1990s and were commonly used by financial institutions.

2. He Was Betting Against CDOs — Not Just Mortgages

The film simplifies the target of Burry’s trades.

In reality, he focused heavily on complex CDO structures rather than basic mortgage bonds.

3. He Was Already Extremely Successful

The film emphasizes his eccentric personality but underplays how successful he already was before 2008.

By the time he began shorting the housing market, he was already managing hundreds of millions of dollars.

4. The Strategy Was Incredibly Expensive

One of the least discussed realities was the cost of maintaining the CDS positions.

Burry reportedly paid between $80 million and $90 million annually in premiums while waiting for the collapse to happen.

If the housing market had stayed irrational longer, the strategy could have failed despite his analysis being correct.

Cornwall Capital: The Most Underrated Trade of the Crisis

One of the lesser-known groups featured in the movie was Cornwall Capital.

Instead of buying protection on the riskiest mortgage assets, Cornwall targeted higher-rated tranches such as A and AA securities.

Because these were considered safer, the insurance premiums were much cheaper.

That allowed them to purchase enormous exposure with relatively little capital.

As panic spread through the financial system, those contracts became extraordinarily valuable.

Some analysts consider Cornwall’s strategy one of the smartest asymmetric trades of the entire crisis.

Why The Big Short Still Matters Today

The relevance of The Big Short goes far beyond the 2008 housing collapse.

The story exposed:

hidden leverage

systemic fragility

blind faith in ratings agencies

financial engineering

moral hazard

excessive risk-taking inside major institutions

It also demonstrated how difficult it can be for markets to recognize obvious structural problems during periods of speculation and easy money.

Even today, investors continue debating whether similar risks could emerge in:

commercial real estate

private credit markets

AI speculation

sovereign debt

shadow banking systems

That is why the story remains so important for modern investors.

Final Thoughts

What made The Big Short so powerful was not simply that a few investors predicted the crash.

It was that they understood the structure of the system better than the institutions running it.

The 2008 crisis was not caused by a single bad investment.

It was caused by layers of leverage, misplaced trust, flawed incentives, and the belief that housing prices could never fall nationwide.

Understanding those mechanisms remains one of the most valuable lessons in modern financial history.

Recommended Reading

For readers interested in understanding the real mechanics behind the 2008 financial crisis, one essential book is The Big Short: Inside the Doomsday Machine by Michael Lewis.

The book goes far deeper than the movie, explaining how Wall Street built an incredibly fragile financial system around mortgage-backed securities, derivatives, and excessive leverage. It is widely considered one of the best modern books on financial crises, market psychology, and systemic risk — especially for investors interested in macroeconomics, banking, and geopolitics.

Link: https://amzn.to/49ByNgy