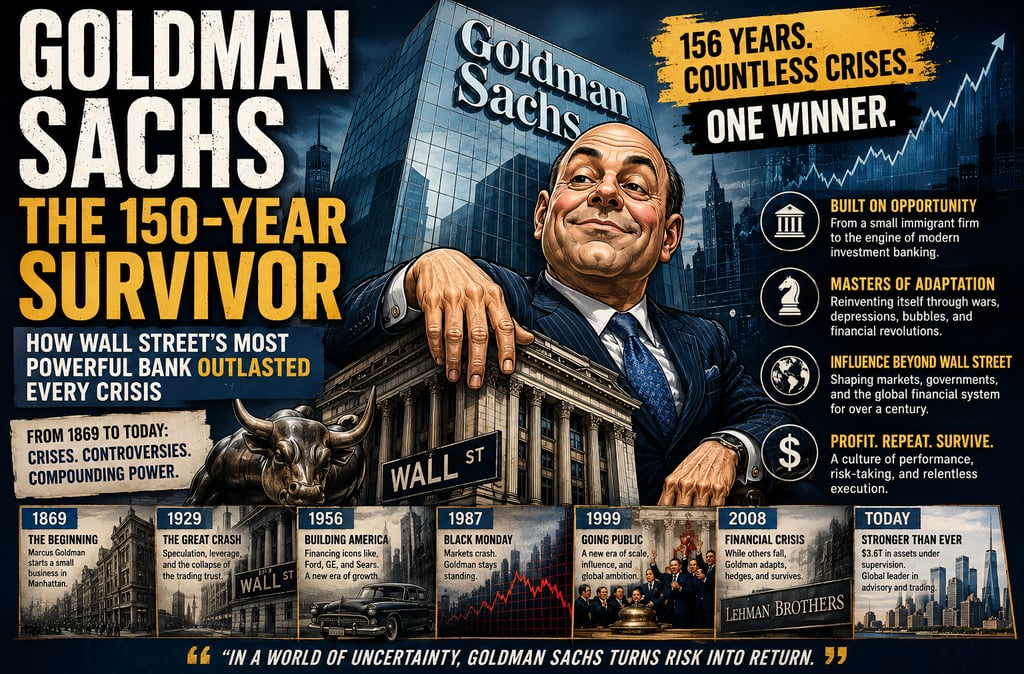

Goldman Sachs History: How Wall Street’s Most Powerful Bank Survived Every Crisis

Inside Goldman Sachs’ 150-year rise through crises, leverage, trading, and global finance dominance on Wall Street.

5/23/20266 min read

Goldman Sachs: The 150-Year Evolution of Wall Street’s Most Efficient Power Machine

Few financial institutions survive for more than a century. Fewer still emerge from every major economic crisis stronger, richer, and more influential than before. Yet Goldman Sachs has done exactly that.

From the industrial boom of post-Civil War America to the collapse of the global financial system in 2008, Goldman repeatedly adapted faster than competitors, identified structural shifts before the market consensus, and institutionalized a culture built around one principle: performance above all else.

Its history is not simply the story of an investment bank. It is the story of modern American capitalism itself — industrialization, financial engineering, leverage cycles, globalization, deregulation, and the fusion of Wall Street with political power.

The central tension that defines Goldman Sachs has remained remarkably consistent for more than 150 years:

How far can financial intelligence scale before it becomes indistinguishable from institutionalized greed?

The Origins of Modern Investment Banking

Marcus Goldman arrived in New York in 1869 during one of the most transformative periods in US economic history.

America was rapidly industrializing:

Railroads connected the continent

Steel and oil industries exploded

Immigration accelerated labor expansion

Capital markets began integrating nationally

Unlike traditional commercial banks, early investment banking firms specialized in higher-risk financing structures. Goldman entered the market through commercial paper — short-term corporate debt instruments.

His model was straightforward but innovative:

Purchase promissory notes from merchants at a discount

Resell them to investors at a markup

Profit from liquidity intermediation

Within a decade, Goldman reportedly handled roughly $30 million annually in commercial paper transactions — an enormous figure for the era.

When his son-in-law Samuel Sachs joined the business in 1882, the firm adopted the name that would eventually dominate Wall Street.

Goldman Sachs and the Democratization of IPOs

At the end of the 19th century, underwriting public offerings became the most lucrative segment of finance.

The market, however, was controlled by elite banking houses such as JPMorgan Chase, whose networks were deeply tied to old European capital.

Henry Goldman recognized an opportunity ignored by the financial establishment:

Retail businesses

Industrial companies

Jewish-owned enterprises excluded from traditional banking networks

This strategic positioning reshaped investment banking.

Most importantly, Henry Goldman helped popularize a revolutionary concept for equity valuation: pricing companies based on earnings power rather than only physical assets.

That framework eventually evolved into the modern price-to-earnings ratio (P/E), now foundational to global equity analysis.

The 1906 IPO of Sears became a turning point:

It proved retail corporations could command institutional capital

It expanded the universe of investable public companies

It elevated Goldman into the first tier of American finance

This period also marked the growing institutionalization of US financial markets, including the creation of the Federal Reserve in 1913.

The First Major Collapse: Speculation and the Great Depression

By the 1920s, America entered an unprecedented speculative boom.

Financial leverage surged. Equity markets became euphoric. Investors increasingly believed economic growth was structurally permanent. Under the aggressive leadership of Waddill Catchings, Goldman embraced increasingly leveraged investment vehicles.

The firm launched the Goldman Sachs Trading Corporation in 1928:

Goldman contributed roughly $1 million in equity

The public supplied approximately $93 million

The structure amplified returns through leverage and speculation

Timing could hardly have been worse.

When the 1929 crash hit:

Share prices collapsed

Leverage imploded

Investor wealth evaporated

Goldman’s reputation was severely damaged

The episode established a recurring pattern in the firm’s history:

Goldman often thrived during speculative expansions precisely because it was willing to operate near the edge of acceptable risk.

Sydney Weinberg and the Reinvention of Goldman Sachs

After the Great Depression, Goldman required more than survival — it needed legitimacy. That rebuilding effort centered around Sidney Weinberg.

Weinberg’s rise became part of Wall Street mythology:

He entered the firm as a janitor

Left school early to support his family

Eventually became Goldman’s dominant power broker

More importantly, he rebuilt client trust.

During the 1930s and post-war era, Weinberg transformed Goldman into a premier advisory institution for corporate America.

Key achievements included:

Advising General Electric

Leading the IPO of Ford Motor Company in 1956

Expanding Goldman’s access to industrial America

The Ford IPO was especially symbolic.

For decades, Henry Ford distrusted Wall Street and openly embraced antisemitic views. Goldman’s eventual selection for the offering reflected how indispensable the firm had become.

The Rise of Trading Culture

During the postwar decades, Goldman evolved beyond traditional investment banking. Under Gus Levy, trading became central to the firm’s identity.

Levy pioneered block trading strategies:

Buying large discounted share blocks privately

Gradually selling them into public markets

Capturing arbitrage spreads

This transformed Goldman culturally and financially.

Historically, traders occupied lower status than corporate bankers inside elite firms. Levy changed that hierarchy permanently.

The implications were profound:

Risk-taking gained institutional prestige

Trading revenues became strategically central

Goldman developed a more aggressive internal culture

The modern Wall Street model — where trading desks rival advisory divisions in influence — owes much to this transition.

Institutional Discipline and the “Goldman Culture”

After Levy’s death, leadership passed to John Whitehead and John Weinberg. Whitehead introduced what became known as the “14 Principles” of Goldman Sachs.

The most important principle: “Our clients’ interests always come first.”

This was not merely branding. It was institutional risk management. Goldman had nearly collapsed twice because short-term incentives overwhelmed long-term trust.

The new culture emphasized:

Extreme internal discipline

Partnership accountability

Long-term client relationships

Meritocratic competition

This environment later produced an extraordinary network of policymakers and financial leaders, including:

Mario Draghi

Mark Carney

Robert Rubin]

Goldman became more than a bank. It became an elite training institution for global financial governance.

Deregulation, Financial Engineering, and the Speculative Machine

The 1980s fundamentally reshaped global finance.

Key macro drivers included:

Financial deregulation

Lower capital restrictions

Rapid growth in derivatives markets

Expanding M&A activity

Global capital liberalization

Goldman thrived in this environment.

Under Robert Rubin, the firm aggressively expanded:

Options trading

Risk arbitrage

Proprietary trading

Structured finance

By the early 1990s, trading profits increasingly dominated earnings.

This transition mirrored a broader structural shift across Wall Street: Finance was moving away from relationship banking and toward balance-sheet-driven speculation.

LTCM and the First Warning About Systemic Fragility

The collapse of Long-Term Capital Management in 1998 exposed the fragility of highly leveraged financial engineering.

The hedge fund employed:

Nobel Prize-winning economists

Advanced quantitative models

Massive leverage

Complex fixed-income arbitrage strategies

When Russia defaulted on sovereign debt in 1998, LTCM’s models failed catastrophically.

Goldman’s response was revealing:

The firm rapidly unwound exposures

Market participants accused Goldman of exploiting privileged information

The Federal Reserve coordinated a rescue to prevent systemic contagion

The episode foreshadowed the moral hazard dynamics that would later define the 2008 financial crisis.

IPO, Public Markets, and the End of the Old Partnership Model

In 1999, Goldman Sachs went public. The IPO represented a historic structural shift:

Before:

Partners risked personal capital

Incentives were closely aligned with firm survival

After:

Public shareholders absorbed risk

Scale became easier

Compensation incentives changed

The transition reflected broader trends in global finance:

Institutionalization of capital markets

Expansion of publicly traded financial conglomerates

Increased dependence on leverage and trading

Goldman’s public listing also revealed the extraordinary profitability accumulated during the 1990s technology and derivatives boom.

The 2008 Financial Crisis: Survival Through Positioning

The defining moment of modern Goldman Sachs came during the subprime crisis. Between 2005 and 2007, Wall Street aggressively securitized low-quality mortgage debt into mortgage-backed securities (MBS).

Goldman participated heavily in underwriting and distributing these products.

But internally, some analysts concluded the housing market was fundamentally unstable.

The firm began reducing exposure and purchasing credit default swaps (CDS) — effectively betting against the same mortgage ecosystem it had helped create. This remains one of the most controversial chapters in Goldman’s history.

Critics argued:

Goldman profited from products sold to clients

Conflicts of interest became systemic

Client alignment had deteriorated

Defenders argued:

Risk management required hedging deteriorating exposures

Survival depended on adaptability

Markets reward correct positioning, not loyalty to consensus

When the crisis escalated:

Lehman Brothers collapsed

Bear Stearns disappeared

Global credit markets froze

Goldman survived through a combination of:

Faster risk recognition

Federal Reserve liquidity access

Emergency capital

A critical $5 billion investment from Berkshire Hathaway led by Warren Buffett

Buffett’s investment provided more than capital. It restored confidence. In crisis environments, perception itself becomes liquidity.

Goldman Sachs Today: Scale, Influence, and Strategic Refocus

Under David Solomon, Goldman largely abandoned attempts to become a mass-market retail bank.

Instead, it returned to its historical strengths:

Mergers & acquisitions

Institutional trading

Asset management

Capital markets advisory

Key metrics cited in the source material include:

$53.5 billion in net revenue in 2024

Approximately $14 billion in profit

Around $3.6 trillion in assets under supervision

Continued global leadership in M&A advisory

Strategically, Goldman now operates less like a traditional commercial bank and more like a hybrid institution combining:

Elite advisory capabilities

Hedge-fund-style trading sophistication

Global asset management scale

Deep political connectivity

The Core Lesson of Goldman Sachs

The history of Goldman Sachs ultimately reflects a deeper truth about financial capitalism:

Markets do not consistently reward morality. They reward adaptability, information, speed, and survival.

Across wars, depressions, crashes, scandals, and regulatory cycles, Goldman repeatedly demonstrated four institutional advantages:

Rapid strategic repositioning

Aggressive talent selection

Exceptional risk culture

Relentless operational efficiency

Its critics view the firm as the embodiment of financial excess and elite capture. Its defenders view it as the most sophisticated risk-management institution ever built. Both perspectives may be true simultaneously.

What remains undeniable is that Goldman Sachs helped shape the architecture of modern global finance — and continues to influence the relationship between markets, governments, and capital allocation across the US and Europe.

Recommended Reading

For readers seeking a deeper understanding of Wall Street culture, institutional risk-taking, and the evolution of modern finance, one of the most relevant books is: The Partnership by Charles D. Ellis

The book offers one of the most detailed historical analyses of Goldman Sachs’ internal culture, leadership structure, and transformation from private partnership to global financial powerhouse.

Link: https://amzn.to/3PGTDEB