Global Fertility Collapse: The Hidden Macro Shock Reshaping the US, Europe, and Financial Markets

A deep macroeconomic analysis of global fertility decline, its impact on US and European economies, Social Security, labor markets, Wall Street pricing, and long-term sovereign risk. An investor-focused breakdown of the demographic slowdown reshaping global growth.

6/24/20263 min read

The Global Fertility Collapse: The Macro Shock Wall Street Is Still Underestimating

A boots-on-the-ground perspective reveals a structural force quietly reshaping developed economies: fertility collapse. This is not a cyclical trend. It is a multi-decade demographic unwind that is already embedded in the fiscal trajectory of the United States, Europe, and Japan.

The evidence suggests that markets are still mispricing the second and third-order effects of aging societies—especially on labor supply, sovereign debt sustainability, and long-duration asset valuations.

The Demographic Time Bomb Markets Are Pricing Wrong

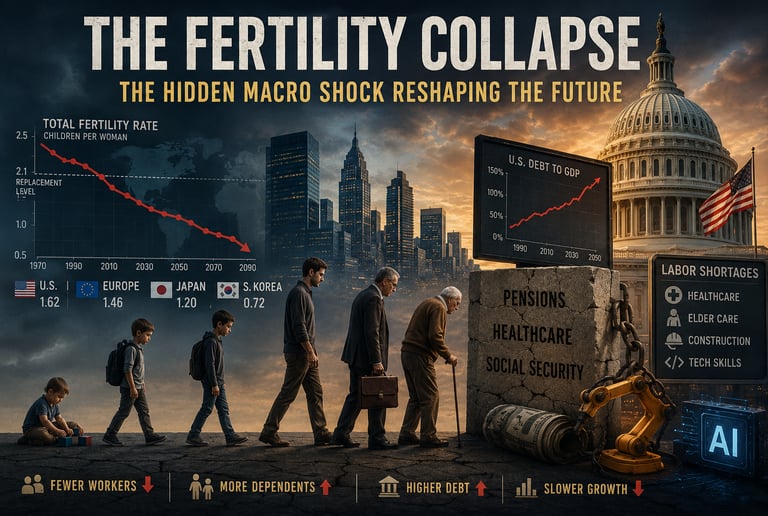

The core issue is simple but brutal: developed economies are no longer replacing themselves. Fertility rates across the US and Europe are persistently below the replacement threshold (~2.1 children per woman), and in many cases collapsing toward 1.2–1.6.

What this means in practice:

Fewer workers entering the labor force each year

A rapidly expanding retiree cohort drawing on public systems

Shrinking tax bases supporting expanding entitlement obligations

Rising dependency ratios (fewer workers per retiree)

In the United States specifically:

Social Security and Medicare are increasingly funded on an unsustainable pay-as-you-go model

The labor market depends more heavily on immigration and automation to maintain growth

Real GDP growth becomes structurally harder to sustain without productivity shocks

This is not a future problem. It is already embedded in fiscal projections.

Why Fertility Collapse is a Sovereign Balance Sheet Problem

At its core, this is not a “social trend.” It is a sovereign balance sheet deterioration.

Governments were built on an implicit assumption: A growing population of workers finances a smaller retired population. That assumption is breaking.

Key macro pressures:

Entitlement systems (US Social Security, Medicare) face long-term funding gaps

Defense spending rises as a share of GDP without expanding tax bases

Interest costs compound faster as debt rolls into a slower-growth economy

Bond markets begin to reprice “growth scarcity risk”

The bond market implication is critical: lower structural growth does not automatically mean lower yields if fiscal deficits widen faster than the demographic drag.

The Failed Playbook: Cash Incentives Don’t Reverse Demographics

Governments have tried to fight fertility decline with financial incentives. The pattern is consistent: temporary bumps, no structural reversal.

A boots-on-the-ground perspective from multiple developed economies suggests the same outcome:

Short-term fertility increases when subsidies are introduced

Long-term decline resumes once incentives lose marginal impact

Most programs simply accelerate timing of births, not total births

Hungary is a frequently cited case:

Aggressive family subsidies and tax incentives

Short-term rise in fertility rates from extremely low levels

Partial reversal later as structural forces reasserted themselves

The key takeaway for US/EU policymakers is uncomfortable: fiscal incentives can shift timing, but they do not override deep behavioral and cultural constraints.

Why Money Doesn’t Fix It: The Structural Drivers

The evidence suggests fertility decline is not primarily a financial constraint. It is a lifestyle equilibrium shift.

Key drivers in the United States and Europe:

Housing costs in major cities (NYC, San Francisco, London) distort family formation

Career acceleration penalties for early parenthood, especially for women in high-skill labor markets

Increased opportunity cost of time in knowledge economies

Delayed adulthood milestones (marriage, home ownership, financial stability)

Cultural redefinition of fulfillment away from family-centric models

Put simply:

In modern urban economies, children are no longer an economic necessity—they are an optional, high-cost life choice competing with career and consumption.

Market Implications Wall Street Is Not Fully Pricing In

This demographic shift is not just a social issue. It is a multi-asset macro driver. Where the impact shows up:

Labor markets

Structural wage pressure in low-skill sectors

Increased reliance on immigration policy cycles

Persistent shortages in healthcare, elder care, and logistics

Equity markets

Automation beneficiaries (robotics, AI, industrial software)

Healthcare and senior services expansion plays

Underperformance risk for domestic consumer growth models

Fixed income

Higher long-term fiscal risk premiums

Volatility in long-duration sovereign bonds

Potential for “growth scarcity” to replace inflation as the dominant macro narrative

Real estate

Aging societies shift demand from expansion to replacement

Secondary cities may outperform global mega-cities in relative affordability terms

The Real Constraint: Culture, Not Capital

The key misunderstanding in policy circles is the belief that fertility is a financial engineering problem.

It is not. The evidence suggests that fertility behavior is now driven by:

Identity and lifestyle preferences

Institutional incentives embedded in education and labor markets

Perceived geopolitical and economic uncertainty

The psychological cost of long-term responsibility in unstable systems

Even strong fiscal incentives tend to attract:

Couples already planning children

Timing shifts rather than net increases

Regional effects (rural > urban response)

Urban centers in the US and Europe remain structurally resistant to fertility recovery because they maximize opportunity cost of childbearing.

Policy Direction in Washington and Europe

Expect policy convergence in three areas:

Expanded child tax credits and family subsidies

Immigration normalization as a labor force stabilizer

Heavy investment in automation and productivity offsets

However, the underlying tension remains unresolved:

Immigration solves labor shortages, but creates political friction

Subsidies are fiscally expensive and only partially effective

Automation offsets labor decline but does not restore population-driven demand growth

This is a system being managed, not fixed.

Final Investor Take

From an investor’s perspective, this is one of the most important slow-moving macro trends of the century.

The portfolio implications are not theoretical—they are already emerging in sector rotation, fiscal behavior, and long-term growth expectations.

The key question is not whether fertility will recover in developed markets. It is whether markets are correctly pricing a world where it does not.

Right now, the answer is likely no.