Geopolitical Fragmentation Is Reshaping Markets: Iran, Ukraine, Europe's Demographic Crisis and the New Global Order

From Iran-U.S. tensions and Ukraine's defense challenges to Europe's aging population and the rise of alternative global institutions, discover the geopolitical forces reshaping markets, energy, defense spending, and investment opportunities in 2026.

6/1/20265 min read

The New Age of Fragmentation: Why Investors Should Pay Attention to Iran, Ukraine, Europe’s Demographic Crisis, and the Rise of Parallel Institutions

Global investors are increasingly facing a reality that few portfolio models were designed to handle: simultaneous geopolitical fragmentation across multiple regions.

From tensions in the Middle East and the ongoing war in Ukraine to Europe's demographic decline and the emergence of alternative global governance structures, the evidence suggests that the post-Cold War era of relative stability is giving way to a far more volatile and unpredictable world.

For investors with capital at risk, these developments are not merely political headlines. They are signals that will shape energy markets, defense spending, supply chains, commodity flows, inflation, and ultimately asset prices for years to come.

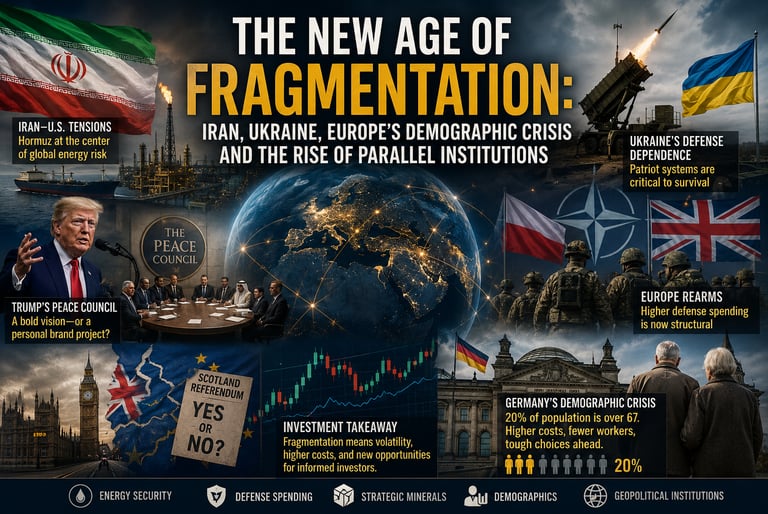

Iran and the United States: A Peace Proposal That Reveals Deep Distrust

A boots-on-the-ground perspective reveals a striking contradiction in the latest reports surrounding negotiations between Washington and Tehran.

Iranian officials have reportedly outlined a draft proposal involving a ceasefire framework, security arrangements around the Strait of Hormuz, and potential changes in regional military positioning. Yet public statements from both sides remain sharply at odds.

The proposed framework allegedly includes:

Reduced U.S. military presence near Iranian territory.

Restoration of commercial traffic through the Strait of Hormuz.

Joint oversight mechanisms involving regional actors.

Discussions regarding Iran's enriched uranium stockpile.

However, significant obstacles remain.

Washington continues to insist on maintaining pressure through sanctions and securing guarantees regarding Iran's nuclear capabilities. Meanwhile, Iranian leadership has publicly rejected any transfer of enriched uranium outside the country.

That contradiction matters. Markets often focus on whether negotiations exist. Investors should focus on whether the incentives behind those negotiations actually align. Right now, they do not.

Why Hormuz Matters More Than Most Investors Realize

The Strait of Hormuz remains one of the world's most important strategic chokepoints.

Any disruption affects:

Global oil prices.

LNG shipments.

Insurance costs for maritime transportation.

Energy-intensive manufacturing industries.

Inflation expectations across developed economies.

Even if military escalation is avoided, uncertainty itself acts as a tax on global commerce.

For investors, this means energy volatility remains a structural feature rather than a temporary event.

Ukraine's Growing Dependence on Western Air Defense

While Ukraine has demonstrated increasing capability through long-range drone operations, a less discussed reality is emerging.

The country's ability to withstand future Russian missile campaigns remains heavily dependent on Western air-defense systems.

Particularly important are:

Patriot missile batteries.

Radar systems.

Interceptor stockpiles.

NATO logistical support networks.

The geopolitical debate is no longer about whether Ukraine receives support.

The debate is increasingly about who pays. The current U.S. position appears to favor a model in which European allies finance military purchases while American defense contractors supply the equipment.

That arrangement creates a fascinating investment implication.

Europe's Rearmament Is Becoming Structural

Poland and the United Kingdom continue expanding military cooperation focused on:

Air-defense integration.

Cybersecurity.

Intelligence sharing.

Defense technology development.

At the same time, policymakers across Europe increasingly frame Russia as a long-term security threat. Whether one agrees with that assessment or not is secondary.

What matters for markets is that governments are budgeting accordingly. Defense spending is evolving from a temporary response into a multi-decade fiscal commitment.

For investors, this supports a bullish long-term case for:

Aerospace manufacturers.

Missile-defense companies.

Cybersecurity providers.

Strategic infrastructure firms.

The Emerging Battle for Rare Earth Dominance

One of the most underappreciated geopolitical stories is the growing competition over rare earth minerals. Washington's strategic objective is increasingly clear: reduce dependence on Chinese supply chains.

Rare earths are critical for:

Electric vehicles.

Advanced semiconductors.

Military hardware.

Artificial intelligence infrastructure.

Renewable energy systems.

The next decade may not be defined by competition for oil alone. Instead, strategic minerals could become the foundation of economic power.

Investors who continue viewing commodities through a twentieth-century lens risk missing one of the most significant shifts in global resource allocation.

Trump's Peace Council: A New Institution or a Personal Brand Project?

Perhaps the most intriguing development is the proposal for a new international peace framework associated with Donald Trump.

The initiative reportedly seeks to participate in post-war reconstruction efforts, particularly in Gaza, where rebuilding costs are estimated in the tens of billions of dollars.

The broader ambition appears even larger. Supporters envision an alternative diplomatic platform capable of operating outside traditional institutions.

Critics see a different picture.

They argue the project is overly dependent on a single political figure and lacks the institutional legitimacy necessary for long-term influence.

The early warning sign is funding. Despite ambitious announcements, reported financial commitments have not yet translated into meaningful capital contributions.

In markets, credibility is measured by execution. The same rule applies to geopolitics. Without sustained financial support and broad international participation, alternative institutions often remain headlines rather than history.

Brexit's Long Shadow Is Still Reshaping Europe

Many investors assumed Brexit became irrelevant once the initial economic adjustments were absorbed.

That assumption appears increasingly questionable. Scotland's renewed push for another independence referendum highlights a reality that many policymakers underestimated.

Political consequences often outlast economic ones.

The Fragmentation Risk

The United Kingdom now faces overlapping pressures:

Slower economic growth.

Regional political tensions.

Questions regarding future European integration.

Renewed Scottish independence movements.

The evidence suggests Brexit was not an endpoint.

It was the beginning of a longer process of constitutional and political realignment.

Markets generally underestimate slow-moving political risks until they suddenly become urgent.

Germany's Demographic Crisis Is Becoming a Fiscal Crisis

Perhaps the most important long-term story in Europe is not defense, energy, or trade. It is demographics. Germany's aging population is creating mounting pressure on social programs, healthcare systems, and public finances.

Policymakers are increasingly exploring ways to redistribute the financial burden associated with demographic decline.

Current debates include higher contributions to long-term care programs and additional incentives for families with children.

The Real Economic Question

The issue extends far beyond Germany.

Most developed economies face the same challenge:

Fewer workers.

More retirees.

Higher healthcare costs.

Slower productivity growth.

The uncomfortable reality is that modern welfare systems were built for growing populations.

Many developed nations now face shrinking or stagnant populations instead.

This is not a cyclical problem.

It is a structural one.

And structural problems tend to become the dominant economic stories of entire generations.

What Investors Should Watch Next

The common thread connecting Iran, Ukraine, Europe's military buildup, demographic decline, and alternative diplomatic institutions is fragmentation. The world is becoming less centralized, less predictable, and more expensive to secure.

Investors should monitor:

Energy supply disruptions.

Defense spending trends.

Rare earth supply chains.

European demographic policies.

Emerging geopolitical institutions outside traditional frameworks.

The next decade may reward investors who understand geopolitics as deeply as they understand earnings reports.

Because increasingly, geopolitics is becoming earnings reports.

For readers interested in exploring these themes more deeply, one highly recommended book is The End of the World Is Just the Beginning by Peter Zeihan. The book examines how demographics, deglobalization, supply chains, energy security, and geopolitical fragmentation are reshaping the global economic order—many of the same forces now driving today's investment landscape.

Link: The End of the World Is Just the Beginning by Peter Zeihan