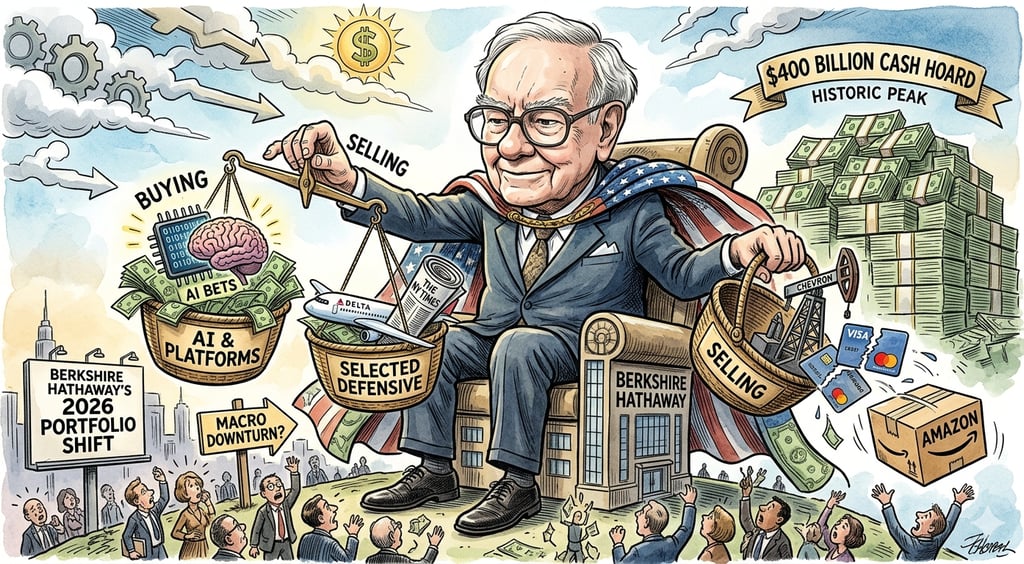

Berkshire Hathaway 2026 Portfolio Shifts: Buffett’s $400B Cash Hoard and AI Investment Strategy

Berkshire Hathaway reshapes its 2026 portfolio with Alphabet, Delta, and NYT buys while trimming Visa, Amazon, and Chevron amid record $400B cash.

5/24/20263 min read

Berkshire Hathaway’s 2026 Portfolio Shift: Buffett’s Cash Hoard, AI Bets, and Strategic De-Risking

The latest disclosed movements at Berkshire Hathaway have reignited a recurring Wall Street debate: is the conglomerate preparing for a macro downturn, or simply rotating capital into higher-quality, long-duration compounding assets?

In Q1 2026, the portfolio managed historically by Warren Buffett shows a clear pattern: aggressive trimming of select financial and energy exposures, alongside increased conviction in AI-linked platforms and select defensive media and aviation names. At the same time, Berkshire’s cash position has reached a historic peak of roughly $400 billion, intensifying speculation across US and European markets about forward-looking macro risk.

1. Berkshire Hathaway in Context: Scale, Returns, and Relative Outperformance

Historical performance vs US equities

Over multiple decades, Berkshire Hathaway has significantly outperformed the broader US equity market, particularly the S&P 500 benchmark.

Key long-term metrics:

~19% annualized return since 1965 vs ~11% for the S&P 500

~67% cumulative outperformance over the last 20 years (approximate framing from recent commentary)

Recent performance:

Last 12 months: slight underperformance (~-5% range cited)

5-year horizon: still strongly positive (~+67%)

Structural insight (fact-based interpretation)

Berkshire’s return profile reflects:

Insurance float reinvestment advantages

Concentrated long-term equity positions

Opportunistic allocation during market stress (2008, 2020)

2. Portfolio Evolution: From Banks to Tech Concentration

Long-term rotation pattern (historical facts)

Berkshire’s equity book has shifted meaningfully over time:

2010s: Heavy exposure to US banks (notably Wells Fargo)

Mid-2010s: Expansion into consumer staples (Coca-Cola remains core)

2016 onward: Rapid scaling into technology, especially Apple Inc.

Recent years: Gradual reduction in Apple concentration

Apple’s dominance phase

Apple became Berkshire’s largest position

Peak exposure estimated around ~40–50% of equity portfolio at certain points

Partial profit-taking began in 2021–2025 cycle

Interpretation

This evolution reflects a structural shift:

From financial cyclicality (banks)

To consumer defensives (Coca-Cola)

To “capital-light compounders” (Apple, Microsoft-adjacent ecosystem exposure indirectly)

3. Q1 2026 Portfolio Moves: What Berkshire Bought and Sold

3.1 Major additions (facts)

Increased positions:

Alphabet Inc. (+~220% reported increase)

Delta Air Lines (new/renewed accumulation)

The New York Times Company (+~200% increase)

3.2 Major reductions and exits (facts)

Chevron Corporation (-35% reduction)

Visa Inc. (reported full exit)

Mastercard Inc. (reported full exit)

Amazon.com Inc. (reported full exit)

Partial reductions in other financial and industrial exposures

4. Interpreting the Moves: Macro Signals vs Micro Allocation

4.1 Artificial intelligence and platform economics (interpretation)

The increase in Alphabet exposure aligns with structural themes in US tech:

AI-driven cloud demand expansion

Monetization of compute infrastructure via Google Cloud

Search + YouTube cash flow stability

Fact anchor:

Alphabet has reported accelerating growth in cloud revenue and improved profitability, reinforcing its role as an AI infrastructure beneficiary.

4.2 Energy de-risking and oil cycle timing (interpretation)

Reduction in Chevron exposure may reflect:

Profit-taking after oil price spikes

Expectation of normalization in geopolitical risk premiums

Rotation toward lower-input-cost beneficiaries (airlines)

5. The Airline Bet: Delta as a Post-Cycle Play

The renewed interest in Delta Air Lines reflects a classic post-crisis consolidation thesis:

Airline industry post-COVID has structurally reduced competition

Pricing power has improved among surviving carriers

Fuel cost sensitivity remains a dominant earnings driver

Macro interpretation

Berkshire may be positioning for:

Lower oil prices → margin expansion

Continued demand normalization in global travel markets

Oligopolistic airline pricing environment in the US

6. Media as an AI-Winner Hedge: The New York Times Case

The position in The New York Times reflects a broader informational economy thesis:

Subscription-based recurring revenue model

High-margin digital transformation completed post-print decline

Content credibility becomes more valuable in an AI-saturated information environment

Interpretation

In a world of synthetic content:

Trusted information providers gain pricing power

Brand authority becomes a defensive moat

7. Why Berkshire Is Selling: Structural Drivers

7.1 Portfolio management transition (fact-based explanation)

A key structural change is internal:

Departure of portfolio manager Todd Combs (reported)

Redistribution or liquidation of positions tied to his mandate (Visa, Mastercard, Amazon among them)

7.2 Portfolio simplification strategy (interpretation)

The broader pattern suggests:

Reduction of “mid-conviction” positions

Concentration into fewer, higher-conviction macro winners

Preference for cash optionality

8. The Record Cash Position: Signal or Strategy?

Berkshire’s cash reserve has reached approximately $400 billion, the highest level in its history.

8.1 What this means (facts)

Cash is largely held in US Treasury instruments

Rising interest rates have made cash yield more attractive

Capital deployment pace has slowed relative to historical averages

8.2 Market interpretation spectrum

Bullish interpretation:

Waiting for equity market dislocations

Dry powder for large-scale acquisitions

Discipline in overvalued markets

Bearish interpretation:

Limited attractive valuation opportunities

Broader market is structurally expensive

Neutral structural view:

Historically, Berkshire has increased cash before major dislocations (2000, 2008, 2020), but this is not a deterministic predictor of crisis timing.

9. Macro Takeaway: What the Market Should Watch

Key signals from Berkshire’s positioning:

Rotation toward AI infrastructure (Alphabet)

Select cyclical exposure (airlines)

Reduction in payment processors and energy cyclicality

Record liquidity optionality

Investor implications (neutral framing)

US mega-cap tech remains central to long-term capital allocation

Energy exposure may be entering a tactical profit-taking phase

Market leadership may continue concentrating in AI-driven platforms

Cash-rich institutions are maintaining flexibility rather than full deployment

Recommended Book

A highly relevant read for understanding this type of capital allocation mindset is: The Essays of Warren Buffett

It provides direct insight into Buffett’s long-term philosophy on valuation discipline, cash management, and opportunistic investing across cycles.

Link: https://amzn.to/4nVI0q7