AI, Oil, and the Fed: The Hidden Macro Regime Shift Reshaping US Markets in 2026

Global markets are being reshaped by rising US yields, persistent inflation, AI-driven semiconductor shortages, and geopolitical tension in the Middle East. This macro analysis breaks down how the Fed, oil prices, and mega-cap tech concentration are driving a new and unstable investment regime across Wall Street and global equities.

6/22/20264 min read

Global Macro Crossroads: Oil, Rates, and the New AI Liquidity Cycle

The global markets are entering a phase where geopolitics, central bank divergence, and AI-driven capital flows are no longer separate narratives — they are colliding in real time. A boots-on-the-ground perspective reveals something uncomfortable for macro investors: the market is no longer reacting to data, it is reacting to regime shifts.

What we are seeing is not a “soft landing” story. It is a repricing of risk across oil, inflation expectations, and long-duration equity valuations — all at once.

Geopolitics: Peace Expectations vs. Energy Reality

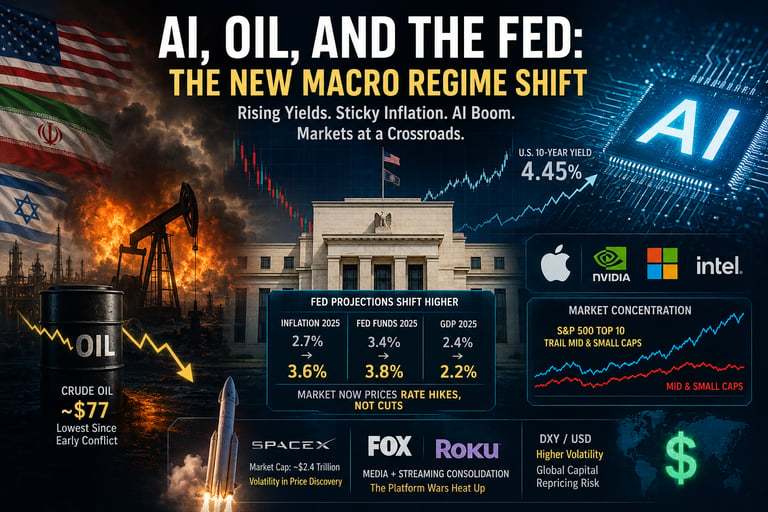

The dominant macro overhang remains the US–Iran–Israel geopolitical triangle, with ceasefire expectations repeatedly delayed.

Fragile de-escalation, unstable pricing

The evidence suggests markets are still pricing an optimistic peace scenario:

Planned US–Iran negotiations in Europe were delayed

Regional tensions between Israel and Lebanon briefly re-escalated

Temporary ceasefire signals reappeared, but without final agreements

Oil briefly retreated toward the $70–$80 range

Crude oil’s reaction matters more than headlines. The market is effectively betting that energy inflation will not re-accelerate. That is a dangerous assumption in a supply-constrained world.

If energy spikes again, the entire soft-landing narrative in the US collapses quickly into a second inflation wave.

The Federal Reserve: From “Higher for Longer” to “Higher Again?”

The most important shift last week came not from geopolitics, but from the Federal Reserve itself — specifically its updated projections. We are no longer in a “rate cut expectation” environment.

Key macro shifts inside the Fed outlook

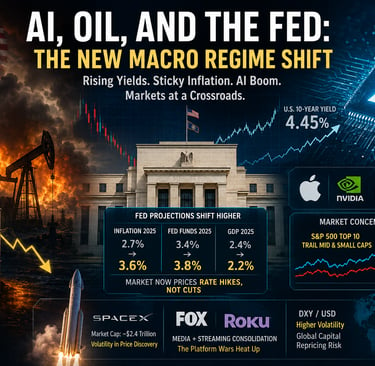

US GDP forecast revised down (≈2.4% → 2.2%)

Inflation forecast revised sharply higher (≈2.7% → 3.6%)

Policy rate projections adjusted upward across 2026–2028

Market pricing shifted toward potential rate hikes, not cuts

The message is blunt: inflation is proving stickier than expected, and the Fed is preparing for structural persistence rather than transitory disinflation.

Long-end yields responded immediately:

US 10-year Treasury moved toward ~4.45%

Term premium is quietly rebuilding

Duration risk is back on the table

This is not the environment investors were positioned for six months ago.

Equities: Liquidity Is Still King, But Narrower Than Ever

Despite macro tightening signals, US equities remain resilient — but increasingly concentrated.

Market performance snapshot

S&P 500: +1.6% weekly, double-digit gains year-to-date

Nasdaq 100: +3.6% weekly, +20%+ YTD

Semiconductor index: +10% weekly, +100%+ YTD

The market is not rising broadly — it is being carried.

The AI Chip Supercycle: Demand Is Breaking Supply Models

The strongest structural force remains AI infrastructure demand. The evidence suggests a supply bottleneck, not just a demand boom:

Semiconductor shortages continue to tighten global supply chains

AI workloads are accelerating capex cycles across Big Tech

Memory chips are becoming the new strategic constraint

Corporate ripple effects

Apple faces rising input costs from chip scarcity

Price increases on future iPhone cycles are being discussed internally

Strategic alignment with Intel signals a partial reshoring of chip dependency

Intel has experienced sharp re-rating momentum on AI supply chain relevance

Apple and Intel are effectively adapting to a world where chip allocation, not demand, is the limiting factor. This is no longer just a tech cycle — it is an industrial constraint cycle.

Mega-Cap Concentration: The Market Is Getting Expensive in the Same 10 Names

One of the most under-discussed signals is valuation dispersion.

Mega-cap tech trades at significantly higher multiples than mid and small caps

Smaller companies remain comparatively undervalued

Capital continues rotating into perceived “safe growth monopolies”

The result is a structural imbalance:

Index performance is strong

Breadth is weak

Opportunity is increasingly hidden outside the top 10 names

This is the kind of setup that works… until it doesn’t.

SpaceX: Private Market Valuations Enter Public Market Psychology

The recent trading debut of SpaceX has introduced a new volatility regime into already stretched risk appetite.

Price action reality check

Initial trading range: sharp surge post-launch

Peak enthusiasm: +30% intraday expansion

Subsequent drawdown: ~15% from highs

Market cap narrative: trillions-level valuation discourse

The critical issue is not whether SpaceX is transformative — it is. The issue is pricing. A boots-on-the-ground perspective reveals a familiar pattern:

Private market narrative gets compressed into public market liquidity

Price discovery becomes sentiment-driven, not cash-flow driven

Volatility increases as institutional anchoring is absent

This is not a traditional IPO dynamic — it is a narrative asset entering liquid markets.

Media and Tech Convergence: Streaming Consolidation Returns

A reported strategic acquisition involving Fox Corporation and Roku reflects a broader theme:

Traditional media is aggressively repositioning into streaming infrastructure

Distribution platforms are becoming more valuable than content libraries

Hardware + software integration is returning as a strategic priority

The market reaction was predictable:

Short-term volatility

Long-term consolidation expectations

We are seeing the streaming wars evolve into platform wars.

The Macro Contradiction: Tightening Rates, Expanding Risk Appetite

This is the core paradox:

The Fed is signaling higher-for-longer (or even higher)

Long-term yields are rising

Inflation forecasts are moving up

Yet equity risk appetite remains aggressive

This divergence is not sustainable indefinitely. Either:

Growth justifies valuations (AI productivity boom), or

Liquidity reprices risk assets downward

There is no neutral outcome in this configuration.

Final Thought: This Is a Market Built on Narrative Compression

We are in a regime where:

Geopolitics drives energy shocks

Energy drives inflation expectations

Inflation drives rates

Rates collide with AI-driven equity concentration and through it all, liquidity keeps selecting the same winners.

A disciplined investor should not confuse momentum with stability. The system is working — until one of these feedback loops breaks.

Book Recommendation

For investors trying to understand how macro cycles, liquidity, and geopolitics intersect with markets, a strong fit is:

“The Alchemy of Finance” by George Soros

It is one of the few works that treats markets not as equilibrium systems, but as reflexive, unstable narratives — which is exactly the regime we are currently in.