AI Infrastructure Investing in 2026: The Hidden Energy, Security, and Workflow Bottlenecks Driving the Next Market Rotation

Wall Street is rotating beneath the surface of the AI trade in 2026, shifting focus from chips and models to infrastructure bottlenecks. This analysis breaks down Zscaler, Vistra, and ServiceNow as key AI-enabling companies tied to security, energy, and enterprise workflows, revealing where institutional capital is moving next.

6/5/20264 min read

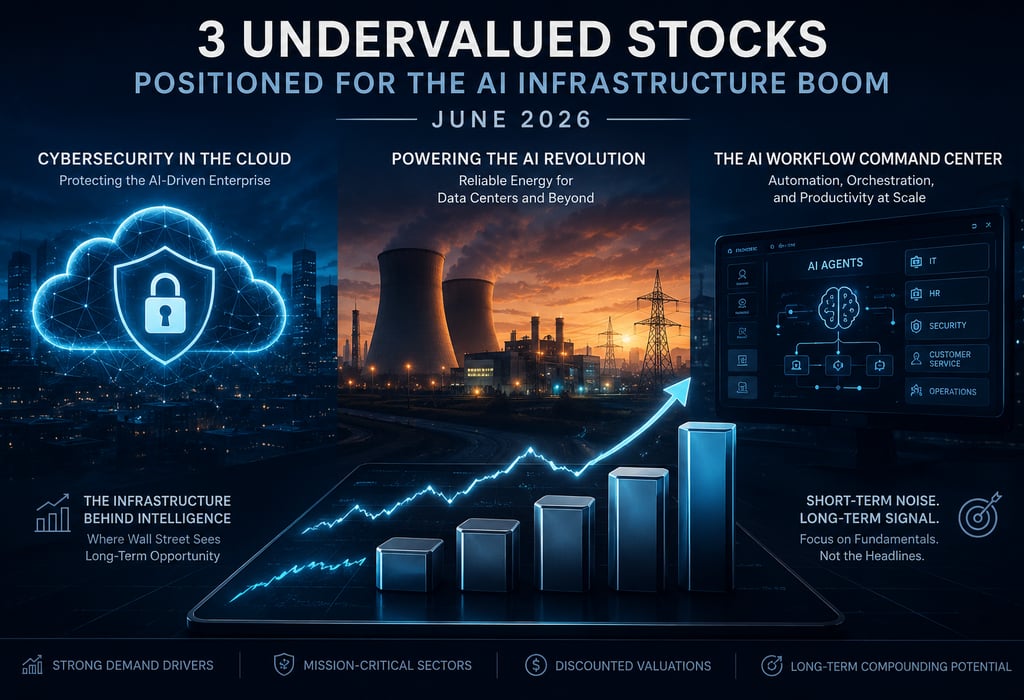

Three “Discounted” AI Infrastructure Plays Wall Street Is Quietly Repricing in 2026

There is a pattern forming under the surface of the AI trade in 2026 that most retail investors are still misreading. The narrative is still obsessed with GPUs, model scale, and frontier labs. But a boots-on-the-ground perspective across Wall Street desks suggests the market is now repricing the plumbing of AI: security, energy, and enterprise orchestration.

The evidence suggests a subtle rotation is underway. Not out of AI—but deeper into the infrastructure that makes AI usable at scale inside Fortune 500 systems.

Below are three companies being framed as “discounted AI infrastructure plays,” each sitting at a different choke point of the AI stack.

1. Zscaler (ZS): The Silent Gatekeeper of the AI Internet

If AI agents become autonomous actors inside enterprise systems, someone has to decide what they are allowed to touch. That is the core thesis behind Zscaler.

The company’s architecture is built around a Zero Trust model: nothing is trusted by default, every request is continuously verified, and traffic is routed through Zscaler’s cloud rather than traditional corporate networks or VPNs.

A boots-on-the-ground perspective reveals why this matters more in 2026 than it did five years ago:

AI agents now generate machine-speed API traffic that no human security team can monitor in real time

Legacy firewall models were built for human users, not autonomous systems

Enterprise attack surfaces expand exponentially when AI tools gain system-level access

Zscaler effectively becomes the “policy layer” between AI agents and corporate data.

What makes the model structurally powerful

Operates across 150+ global data centers

Processes hundreds of trillions of daily security transactions

Built on its own cloud infrastructure rather than relying on hyperscalers

Subscription-based recurring revenue (ARR-driven model)

Key concern from Wall Street:

Growth is decelerating (mid-to-high teens vs ~25% historically)

Market is questioning whether AI platforms eventually bypass traditional security layersc

But here is the counterpoint: AI expansion does not remove security—it multiplies the need for it.

The evidence suggests Zscaler is not being disrupted by AI, but recalibrated by it.

2. Vistra (VST): The Unsexy Bottleneck of the AI Boom

If Nvidia supplies the brain, the real constraint is electricity. That is where Vistra Corp sits in the AI value chain.

Vistra is not a tech company in the traditional sense. It is a large-scale power generator supplying electricity from nuclear, natural gas, and coal assets into the U.S. grid.

The uncomfortable truth emerging in 2026 markets is simple: AI scaling is no longer compute-constrained—it is power-constrained.

Energy mix reality (structural constraint, not marketing)

~62% natural gas

~20% coal

~15% nuclear

~3% renewables

This mix matters because data centers demand:

24/7 uptime

Baseload energy (not intermittent solar/wind dependence)

Long-term contracted pricing stability

And this is where Vistra becomes strategically relevant.

The AI energy trade is becoming contractual

Recent industry dynamics show:

Long-term power contracts tied to AI data center expansion

Partnerships with hyperscalers and AI infrastructure builders

Nuclear capacity increasingly treated as strategic national infrastructure

A key development shaping sentiment:

Large tech firms exploring direct financing of nuclear capacity expansions

That shifts Vistra from a cyclical utility to a quasi-infrastructure proxy for AI growth.

Why the market is still uncertain

Energy regulation risk (especially in U.S. pricing politics)

Capital intensity and leverage exposure

Concerns that AI demand could temporarily overshoot supply commitments

Still, the asymmetry is clear: If AI keeps scaling, electricity demand does not decline—it compounds.

3. ServiceNow (NOW): The Operating System of Corporate Work

While most investors focus on infrastructure and chips, the real monetization layer inside enterprises is workflow automation. That is the domain of ServiceNow.

ServiceNow is evolving from a workflow automation tool into what can only be described as an “AI orchestration layer” for enterprises.

The structural shift happening inside companies

Legacy enterprise environments are fragmented:

ERP systems don’t talk to HR systems

IT tickets live in silos

Workflows depend on email chains and manual routing

ServiceNow connects these systems into a single execution layer. Now the AI layer is being inserted on top of that structure.

The new monetization model: AI tokens + subscriptions

The company is transitioning from:

Traditional SaaS subscriptions

to:Subscription + usage-based AI consumption (tokens)

This matters because:

Revenue scales with AI usage intensity

Enterprise automation becomes consumption-driven rather than seat-driven

Margins can expand if AI workflows scale faster than headcount

Hard data points investors are watching

Revenue growth: ~20%+ range

High recurring revenue retention (~97%+)

Expanding AI segment growth (>100% YoY in recent quarters)

Strong free cash flow generation

Market disconnect

Despite strong fundamentals, the stock has been under pressure, reflecting:

Broader SaaS multiple compression

Uncertainty around pricing transition to AI tokens

Fear of enterprise budget tightening

But the underlying reality is different: AI is not reducing workflow software demand—it is increasing system complexity, which strengthens orchestration platforms.

The Hidden Macro Theme: AI Is Becoming an Energy + Security + Workflow Problem

The common thread across all three companies is not “AI exposure.” It is dependency positioning:

Zscaler → controls access to systems

Vistra → powers the systems

ServiceNow → orchestrates the systems

This is the real AI stack emerging beneath the hype cycle. Wall Street’s rotation is not random. It is moving toward infrastructure that cannot be easily replaced by model improvements alone.

Final Thought: Where This Trade Actually Breaks

The biggest misconception in the AI narrative is that it is a software-only revolution. It is not.

The evidence suggests the binding constraint of AI scaling in the late 2020s will not be intelligence—it will be:

electricity supply

enterprise security architecture

system interoperability

If any of these fail, AI slows regardless of model capability. And that is why capital is quietly flowing into these “unsexy” layers of the stack.

Recommended Reading

A useful framework to understand this shift is “The Innovator’s Dilemma” by Clayton Christensen. It explains why disruptive technologies rarely destroy industries at the top first—but instead reshape the infrastructure and value chains underneath, exactly what we are seeing in AI today.

Link: https://amzn.to/49GcDtV