AI Boom Meets Oil Shock: Inflation Returns as the Fed Loses Control of the Narrative in 2026 Markets

A deep macroeconomic analysis of June 2026 markets covering rising oil prices, re-accelerating inflation, Federal Reserve policy uncertainty, and the AI-driven equity boom led by semiconductor and cloud infrastructure giants.

6/5/20264 min read

Macro Market Crossroads: Oil Shock, AI Mania, and the Fed’s Inflation Trap Heading Into Summer 2026

The first week of June 2026 opens with a market that looks calm on the surface but is structurally tense underneath. A boots-on-the-ground perspective reveals a familiar pattern: risk assets rallying on geopolitical de-escalation while inflation persistence quietly forces the hand of the Federal Reserve.

The evidence suggests we are not in a “soft landing” narrative anymore. We are in a repricing phase where geopolitics, energy, and AI capex are colliding.

1. Iran–U.S. De-escalation: Markets Price in Peace Before It Exists

The market is increasingly convinced that tensions between the United States and Iran are moving toward resolution.

A leaked draft framework reportedly includes:

A 60-day window to reopen strategic maritime routes

Suspension of naval blockades in key energy corridors

Ongoing negotiations over who controls maritime oversight

Nuclear program constraints still unresolved

From a risk desk perspective, this is classic “pricing the headline before the signature.”

What markets are really trading

Lower geopolitical risk premium in crude oil

Expectation of normalized global shipping flows

A temporary suppression of volatility in energy-linked assets

But here is the uncomfortable part: nothing is actually finalized.

2. Oil: The Inflation Trigger That Didn’t Go Away

Crude oil remains the hidden driver of macro uncertainty.

Prices spiked sharply during escalation phases

Recently stabilized near elevated levels around the $80 region

Still significantly above early-cycle 2026 levels (~$60)

A boots-on-the-ground perspective reveals a simple transmission mechanism:

Higher oil → higher input costs → sticky inflation → tighter monetary expectations This is exactly what is now showing up in inflation data.

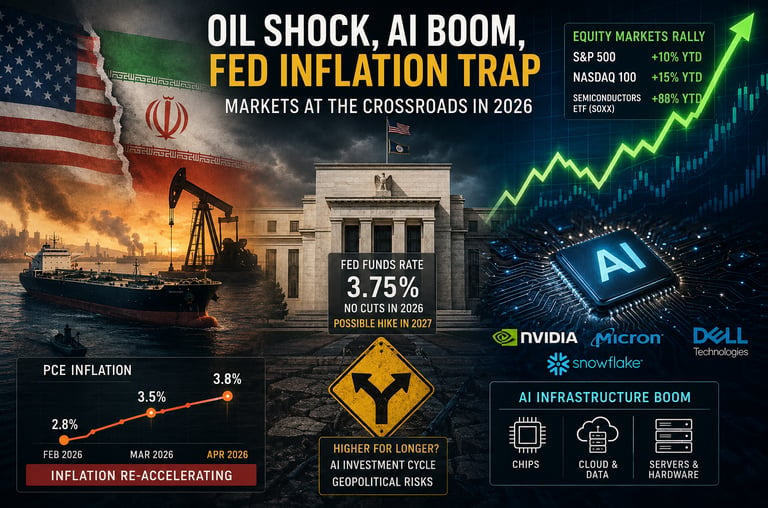

3. Inflation Is Re-Accelerating: The Fed’s Preferred Gauge Is Flashing Red

The key metric is the PCE inflation index, the preferred gauge of the Federal Reserve.

Recent readings:

February: 2.8%

March: 3.5%

April: 3.8%

That is not a rounding error. That is a trend.

Why this matters more than CPI

The Fed focuses on PCE because:

It adjusts for consumer substitution behavior

It reflects broader consumption patterns

It better captures real spending power dynamics

The evidence suggests inflation is no longer “returning to target” smoothly. It is re-anchoring higher due to energy inputs.

4. Interest Rates: The Market Has Given Up on Cuts

The bond market narrative has shifted aggressively.

Current pricing implies:

No rate cuts expected in 2026

Policy rate stable around ~3.75%

Potential tightening cycle resumption by 2027 (toward ~4.0%)

This is the uncomfortable truth Wall Street is slowly absorbing:

The era of easy monetary easing is not guaranteed to return. Instead, the market is now debating:

“How long can rates stay restrictive?”

“Does inflation force another tightening cycle?”

That uncertainty is exactly what compresses valuation multiples over time.

5. Equity Markets: Rallying on Liquidity, Not Clarity

Despite macro tension, equities continue to grind higher.

S&P 500: +10% year-to-date

Nasdaq 100: +15% year-to-date

Semiconductor basket: extreme outperformance

This is not a clean macro rally. It is a liquidity-driven grind supported by AI capex and buybacks. A key structural driver is corporate behavior:

Record share buybacks across tech and industrial sectors

Companies aggressively repurchasing equity during perceived undervaluation windows

Signal: internal management confidence remains strong

But there is a contradiction here:

Earnings expectations are rising

Rates are not falling

Inflation is not fully contained

Something eventually has to give.

6. AI Economy: The New Industrial Core of the Market

The AI trade is no longer speculative. It is now infrastructure spending.

Semiconductor leadership: Micron Technology

Extreme re-rating driven by memory demand cycles

Explosive valuation expansion over the past year

Benefiting from data center bottlenecks and supply constraints

Cloud data layer: Snowflake

Revenue growth ~30% YoY

Strong adoption in AI training pipelines

Consumption-based pricing model tied directly to AI workloads

Infrastructure hardware: Dell Technologies

AI infrastructure revenue growing far faster than legacy PC business

Server demand exploding due to enterprise AI deployment

Guidance implying multi-fold expansion in AI-related revenue streams

The evidence suggests a structural shift: AI is not a sector anymore. It is the backbone of enterprise computing.

7. The Market Paradox: Luxury Branding Meets Structural Risk

Even iconic industrial brands are being pulled into the AI-capital cycle mindset.

Case study: Ferrari

The launch of its first fully electric supercar triggered a divided reaction:

Brand purists rejected the shift away from combustion engines

Investors interpreted it as long-term positioning in electrification

Here is the real tension:

Brand equity vs technological transition

Heritage vs market survival

The stock reaction reflected uncertainty, not fundamentals. A boots-on-the-ground perspective reveals a deeper truth: Even luxury monopolies are not immune to technological regime change.

8. Sector Rotation: Energy and Tech Dominate Everything

Market leadership is highly concentrated: Top performers:

Energy: driven by oil volatility and geopolitical risk premium

Technology: driven by AI infrastructure buildout

Laggards:

Financials

Healthcare

This is not a broad market expansion. It is a narrow thematic regime.

9. Dollar Strength and Global Spillover Risk

Currency markets are also shifting. The U.S. dollar has strengthened again as:

Interest rate expectations remain elevated

Global risk sentiment remains unstable

Capital continues flowing into U.S. assets

This creates a secondary effect:

Pressure on emerging markets

Imported disinflation for Europe

External financing stress in leveraged economies

10. The Real Macro Question for Summer 2026

Strip away the noise and the market is facing three unresolved variables:

Can inflation stay below 4% if oil remains elevated?

Can the Federal Reserve justify rate cuts in a sticky inflation regime?

Can AI-driven earnings growth sustain current equity multiples?

Each answer carries portfolio-level consequences. The uncomfortable reality: Markets are priced for stability, but the macro regime is not stable.

Final Thought: Skin in the Game Perspective

From a risk-taking standpoint, this is not a market to confuse momentum with certainty. Liquidity is still supportive, but macro constraints are tightening underneath.

The winners of this cycle will not just be those exposed to AI—but those who correctly anticipate when inflation forces the Fed to stop accommodating growth narratives.

Recommended Book

For understanding how monetary regimes, inflation cycles, and asset bubbles interact in real markets, a strong reference is:

“Manias, Panics, and Crashes” by Charles P. Kindleberger

It remains one of the clearest frameworks for understanding why markets look rational—right up until they stop being so.

Link: https://amzn.to/4uahFGd